Wealthtime Platform enhancement

Origo’s Unipass LoA service

The Wealthtime Platform has embedded Origo’s Unipass Letter of Authority (ULoA) technology as part of our ongoing digital-first efficiency drive.

Rethinking Retirement

Reassess and find the right solutions for you and your clients

A new phase of retirement planning is on the horizon. That’s why we’ve pooled together the resources from our teams at Wealthtime and Copia, and experts from across the industry.

Data integration

FINIO data hub

Did you know we’ve partnered with Sprint Enterprise to give you access to the FINIO data hub? It connects investment platforms with software providers – providing you with better-quality data and reducing manual inputs. To find out how to set up your feed into your back-office provider, visit our webpage.

Wealthtime Select Platform Enhancement

New: ‘Buy into model’ buttons

We’ve added a brand new feature! It’s a quicker and easier way to invest money into a client’s model, or current investment strategy, without the need to perform a full rebalance.

Wealthtime Platform enhancement

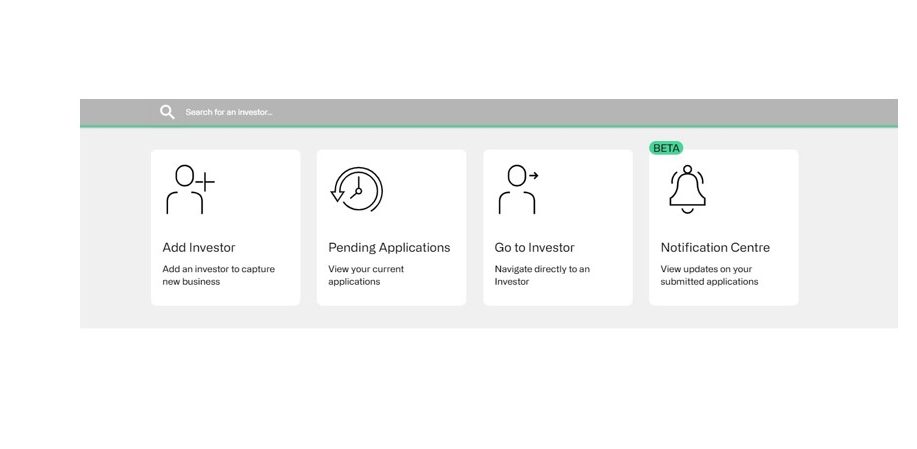

Notifications Centre

Our new Notification Centre has gone live in Adviser Zone. It has replaced the Status Updates section and will now be your one-stop shop for the latest updates on client cases and submissions.

Wealthtime Platform enhancement

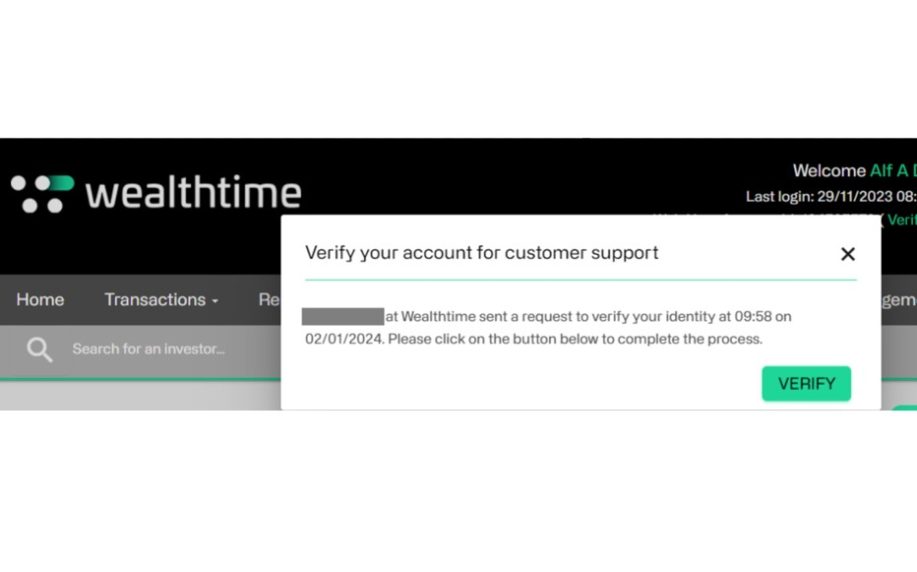

Online verification check

We are introducing new online verification functionality to the Wealthtime Platform to cut the time it takes to complete data protection checks when calling us. The new functionality is available now. It improves on our current process by making things significantly more efficient, whilst maintaining the same high standards of security.

New platform

We’re using innovative solutions and AI to take our platform to the next level.

New possibilities

We believe in keeping pricing simple. You won’t find any hidden fees.

Welcome to the next generation adviser platform business. Here at Wealthtime, you’ll find a smarter technology experience that places you at the core of everything we do.

Following years of hard work and continuous development across two separate platform products, we’ve built a group that’s able to combine top tier technology with a people-centric service. This combination means you can choose which of our two platforms – Wealthtime or Wealthtime Select – best suits you and your clients’ needs. Regardless of which platform you go for, you can take advantage of a service that not only gets the day-to-day essentials right first time, but is also constantly evolving and adapting to change.

We’re always striving to add value and create great outcomes for investors. And as two of the last remaining independent platforms, we’re able to align to your business needs – there’s no direct-to consumer arm or team of advisers competing with you for the same clients.

£11bn

1,500

75,000

One group, two platforms

Wealthtime offers two separate and distinct solutions to satisfy client needs; Wealthtime and Wealthtime Select. Bringing both businesses together under one group name unifies and builds on the strongest aspects of both platforms.

A single group vision allows us to present a seamless and consistent user experience with the best proposition and outcomes for you and your clients.

What we offer you

We can provide you with a comprehensive investment wrap service regardless of which platform you choose. You’ll find everything you’d expect from an advisory platform plus market leading technology and service.

1

2

3

4

Service that truly supports

We want our users to take centre stage. From day one, you’ll get a service that’s designed around you. You’ll know your clients’ investments are protected and you can focus on achieving their desired outcomes. We offer a bespoke and tailored service, named points of contact and full platform training delivered by a dedicated team.

We believe in providing a highly personal service. And part of that is making sure our platforms and technology work to support you and your business now, as well as offer the flexibility required to meet your future needs. We made it our mission from the outset to develop a market-leading, legacy-free platform that makes administration processes easier. All to help you and your business remain productive and efficient, while giving you more time to spend with your clients.

What our technology approach means for you

We know advisers are struggling to create more capacity in their business due to the lack of integration across technology solutions. That’s why we’ve transformed our approach to technology so you benefit from a well-integrated ecosystem and better external data integration. Our combination of GBST, microservices and proprietary technology enables us to continually improve our tools and services. Allowing us to anticipate and rapidly respond to our users’ evolving needs.

Group Awards

Leadership Team

Our Leadership Team reports to our company board and is responsible for all day to day matters of the business. With combined experience of over 175 years and a commitment to excellence, our company culture and adviser experience are in excellent hands. Together they have led the way on the two Wealthtime propositions to ensure our key principle of Pursuing Potential Together is ingrained at every level of the business.

Call our team today

Whether you're looking to start using our service, or simply have a question for us, we're just a phone call or email away. Lines are open 9am to 5pm Monday to Friday. To help us improve our service, we may record or monitor calls.

For Wealthtime platform queries, call

0345 680 8000

For Wealthtime Select platform queries, call

01725 512 925